Written by

13th May 2021 – Written by Imogen Fitt

Key Takeaways:

- Together Siemens-Varian have arguably the broadest in-house product portfolio focused on oncology precision medicine of the major health technology incumbents. Looking ahead, we expect the firm will focus on the use of AI-enabled and digital offerings to guide individualised patients throughout the cancer journey.

- The acquisition is unlikely to signal a wider move in the market towards “closed” or proprietary software provision as providers and regulators increasingly champion the need for interoperability. However, vendors in the market will see increased competition as the newly formed company leverages its formidable sales channels across hardware, software and services.

- Siemens existing relationships with leading healthcare providers for long-term contracting across multiple product sectors should open up C-suite discussions and deals for the Varian Oncology IT portfolio, a route typically harder for a vendor with a singular clinical focus. This may also enable the company to reclaim some of its lost market share in medical oncology information systems from EMR vendors.

Siemens Healthineers officially completed the acquisition of Varian Medical Systems on April 15th 2021. The two companies constitute a combined annual revenue of around $20bn, and there’s little doubt that this decision will have raised eyebrows amongst competitors in the Oncology segment when it was announced back in August 2020.

With the process now complete, in this article we explore how this move will shape the Oncology IT landscape going forward and our expectations for the new expanded Siemens Healthineers.

Building Better

Siemens and Varian have been working together since 2012, when the “EnVision” partnership was first established between the two vendors. Solutions such as ARIA¬Æ connectivity, which enabled Varian’s IT networks to integrate seamlessly with Siemens discontinued linear accelerators, were co-developed. The partnership initially positioned both companies positively, by providing enhanced sales opportunities for new Varian hardware and software deals once linear accelerator replacements were due. This past familiarity should also translate to a relatively smooth transition going forward, though as ever with large corporate mergers of this scale, it will take time for the two firms to realise the benefits of the deal.

Both vendors will be keen to exploit the merger allowing Varian access to Siemens’ much larger operational and sale networks particularly a broader reach across emerging markets where Siemens already has an established presence, especially in emerging Eastern Europe, Middle East, Africa and Asia Pacific markets. In more established markets, the firms are also complementary, with little overlap of Siemens’ own installed base of established customers across Europe and Varian’s strong customer base in the US.

Establishing a Cancer Care Continuum

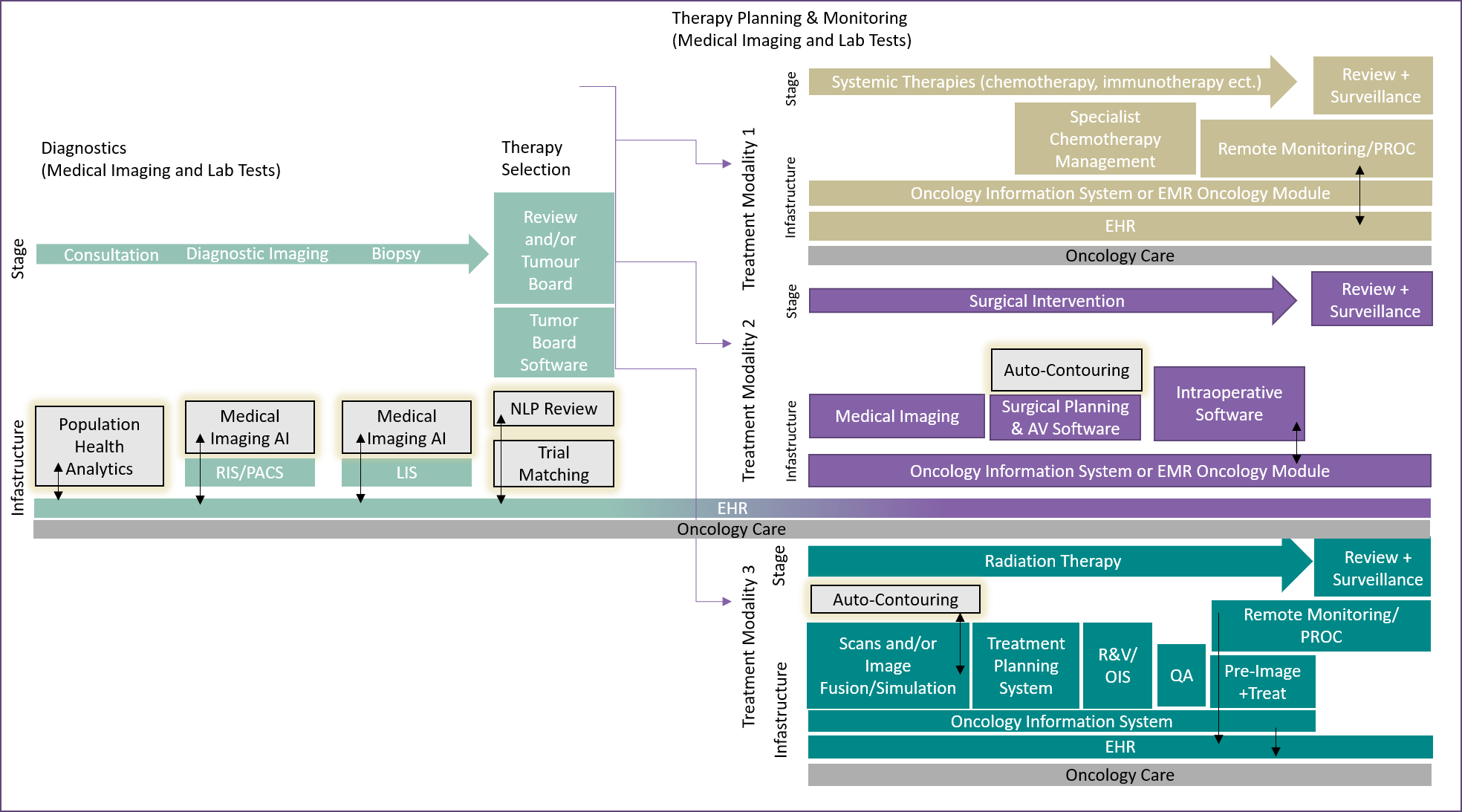

The combined Siemens-Varian oncology portfolio now encompasses most of the Oncology IT workflow for providers (shown in Figure 1).

Although a few larger enterprise products are missing (LIS, EHR) Siemens-Varian now possess broad coverage and knowledge across a range of IT products, which also allows further chances for development across several markets. Further, Siemens still retains a strong relationship with Cerner, one of the leading global EMR vendors, following the spin-off of its Soarian EMR to Cerner in 2014.

The spin-off, along with the Siemens Healthineers IPO and subsequent Varian acquisition, has been part of a long-term strategy for the firm to establish a leadership position in precision medicine. Diagnostics and therapy treatment both involve the use of medical imaging and laboratory tests to enable decisions. Now with a complete imaging portfolio and burgeoning IVD business, the new Siemens-Varian company will be able to start combining and analysing these results, allowing for the development of truly individualised treatment plans, care pathways and AI-enabled clinical decision support tools.

In addition, oncology care contains some of the most complex workflows present in healthcare today, with the discipline moving heavily towards multidisciplinary collaboration. As this practice develops, we expect provider focus to intensify on fixing issues within software interoperability. How Siemens and Varian approach this challenge will be key to long-term success; Siemens has traditionally been slower to move its digital capabilities towards a more consolidated and open-source platform, notably only recently announcing a roadmap to connect its imaging IT solutions together via the syngo Carbon platform. Initially this preponderance will have limited impact, such is the relatively best-of-breed approach to Oncology IT in most markets today – however if Siemens is to realise its precision medicine aims, integration and interoperability for its broader digital portfolio will be critical to success.

Homing in on Emerging Markets

Integration across workflows also leads the way towards clinical pathways and tumour board development, and the company would be very well positioned to integrate information from across products. Competitors in this space are currently immature and often struggle to provide the use-case for their technology. The key challenge in this market therefore, would be replacing existing teleconferencing platforms like Microsoft and Zoom, which have no specialist capabilities but seem to have been adopted widely throughout last year as a COVID-19 solution to continuation of services. These platforms however do not offer benefits to workflow, nor do they facilitate access to a wide range data required for oncology care. Siemens-Varian would therefore be much better positioned to integrate and curate this information easily for providers compared to start-up vendors.

However, we do not think this focus on end-to-end oncology management signals a wider move in the market towards “closed” proprietary software provision. Providers themselves see the benefit in interoperability and vendor neutrality and are increasingly frustrated by complex integrations. Oncology sits at the convergence of many major departmental and enterprise IT systems and historically seen a healthy demand for neutral best-of-breed solutions, such as those provided by vendors like RaySearch Laboratories. RaySearch Laboratories itself has begun some progress in larger academic and cancer centers, through focusing on the provision of AI-enabled software to improve provision across a range of parameters. Navigating this balance between best-of-breed capability and singular platform interoperability and customer retention will be a challenging tightrope to navigate for the firm in Oncology, let along across broader acute provider diagnostics. However, expertise and a strong position in many of the core product segments should provide the firm with an advantage in terms of navigating core customer transition from standalone point solutions towards broader integrated platforms.

Product Development Across a Plethora of Data

Smaller competitors and start-ups will also see increased competition develop as Siemens-Varian begins to expand its provision across the Oncology IT workflow following the acquisition.

Siemens Healthineers has previously been quoted as intending to “leverage AI-assisted analytics to advance the development and delivery of data-driven precision care and redefine cancer diagnosis, care delivery and post-treatment survivorship.” As demonstrated in Figure 1, there are many of points to apply this. Varian has already announced a partnership with Microsoft designed to develop its own AI-based auto-contouring solution, and further interest in adaptive radiotherapy and oncology analytics can be expected. This does however offer vendors like Mirada Medical a reduced pool of potential partners, which will make scaling solutions much harder for small best-of-breed software vendors

Furthermore, Siemens has also been working with recent Microsoft acquisition Nuance on workflow and integration for its AI-tools in radiology for seamless integration of results from its advanced visualisation into Cerner’s EMR. With a vast pool of resources and data available across its newly formed organisation to train algorithms, we expect further announcements in terms of new partnerships and integrations of AI-analysis tools and AI-enabled care pathway tools.

Outside of AI, other key areas of focus for the two vendors will likely include clinical outcome improvements through solutions designed to enable patient-reported outcome measurements and engagement. This opens the door to several other markets as vendors in the space are seeing interest, and revenue, from pharmaceutical vendors engaged in drug development. By providing PROMs, companies can help supplement the therapeutic development process, helping to steer therapy towards even more personalised development.

Entry into the C-suite for Varian Medical

Further benefits in integration will be clear for customers when negotiating multi-modality sales. With the acquisition, Varian Medical can now participate in sales discussions at the C-Suite level, which could offer much larger deals with providers. This will both enable the company to outcompete other vendors with bundled pricing, whilst also opening the door to long term managed service contracts.

Historically, this characteristic has been present in Siemen’s own focus in recent years on large, managed service contracts for medical imaging (see our recent insight here). To providers in today’s market, this ability to streamline complex supply-chains and rely on larger partners to provide more of its modalities, software and service in long-term contracts will be looking an increasingly attractive way to reduce cost and improve efficiency across larger healthcare systems.

Varian has seen its own coverage of the specialised oncology information system (OIS) market falter in recent years, as hospitals started to digitalise patient records and larger businesses like Epic and Cerner expanded coverage to specialised oncology modules. Whilst these solutions are not designed to cover radiation oncology management, they can provide software for the medical oncology workflow. Decisions to adopt these EMR-based clinical module solutions occur at the C-suite level, where cost savings and contract consolidation can be a more prominent concern over retaining established legacy best of breed clinical systems like OIS. However, ongoing competition between EMR vendors and specialist oncology software vendors is likely to remain predominantly in the surgical and chemotherapy management applications, as EMR vendors seem unlikely to develop their own internal radiation oncology solutions.

Conclusion

Assuming minimal difficulties with integration, solving interoperability challenges mid-term and a relatively short transition period, it is already clear Varian will likely benefit from its new home as part of Siemens Healthineers.

Despite COVID-19’s challenging economic legacy, the deal also poses a promising future to providers regarding the wider development of Oncology IT, offering the choice to use one vendor for almost all oncology solutions. How quickly providers shift towards this approach remains uncertain, though current momentum towards consolidated deals for large acute providers suggest this shift is on the horizon.

Competitors in the oncology IT space should take the move as a prompt to start investing in the cohesive provision of oncology care management, whereas competing larger healthcare technology vendors may question if now they should be broadening their own scope across disciplinary workflows. This may prompt more aggressive strategic moves in the sector, either via acquisition of key vendor or technology assets from major healthcare technology vendors, or closer-knit partnerships between competitors of Siemens-Varian to offer a more complete solution set to compete with the new broad Oncology offering at the firm. With a new era of precision medicine beckoning as technology evolves, it’s clear that the Oncology IT segment will be entering a new, digital phase. Siemens has bet big with the Varian deal that having most technology assets under one roof is the way forward – whether this pays off for the firm is not yet clear, but we believe first-mover advantage and its leadership position in other allied sectors gives the deal a good chance of success.

For access to our insight covering Signify Research’s initial analysis of the announcement please click here.