Cleerly’s Reimbursement Milestone | Spironolactone for Alcohol Use Disorder

Share:

Bhvita Jani

Published: October 3, 2022 In The News

30th September 2022, Contribution by Bhvita Jani – Featured on CardiacWire.com

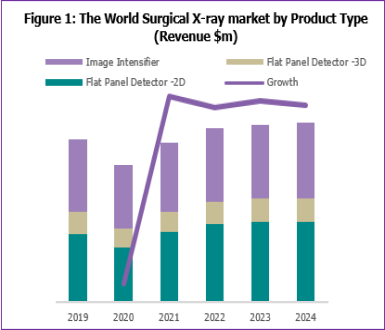

… Interventional X-Ray & Mobile C-Arm Rebound: Signify Research reported strong 2021 rebounds in the interventional X-ray (+10.2%) and mobile C-arm (+15.5%) markets following COVID-related declines in 2020. The firm expects the two interventional segments will see continued (but slower) growth through 2026, with interventional X-ray demand driven by structural heart and neurology procedures, and mobile C-arm growth driven by the aging population and increasing awareness of the benefits of minimally invasive procedures….

You may also like