Written by

Share article:

Co-Written by Arun Gill

Cranfield, UK, October 17th 2022 – The healthcare market is witnessing a dynamic shift in how and where patients want to receive care, with the flexibility and convenience of outpatient settings driving a greater utilisation of outpatient imaging and teleradiology services, a trend most prevalent in the US market. Driven predominantly by changes to reimbursement, and payers pushing non-emergency imaging to the outpatient setting, as well as the legacy of the pandemic having its part to play.

Impacting both image acquisition, image reading, and services, this has led to market growth and vendor opportunities within traditional outpatient imaging providers, such as imaging centres and radiology reading groups, as well as teleradiology groups.

The Importance of Productivity and Efficiency

Despite changes to reimbursement driving patient care towards the outpatient setting, the value of reimbursement (in terms of imaging reads) continues to diminish. Thus, entrenching the importance of products and tools that enrich a provider or radiologists’ efficiency and productivity, whether that is increasing patient throughput, or faster reading and reporting. As such, the outpatient market is, typically, the first to adopt innovative technology, such as AI, analytics and public cloud architecture.

Such innovation paves the way for imaging IT vendors’ future success; to capitalise on this growing market, investment will be required to re-architecture PACS and RIS platforms to utilise the scalability and elasticity of a cloud-native deployment. This demand will continue to intensify as the provider market undergoes further consolidation, and outpatient and teleradiology networks become geographically dispersed. Imaging IT vendors have begun responding to this market trend. Some recent examples include GE HealthCare’s release of TruePACS and Change Healthcare’s launch of the Stratus Imaging platform. However, not all provider needs must be solved natively; for example, in the instance of specialist tools for viewing and reporting, or AI image analysis tools. The route of partnership and direct integration will be preferred by many imaging IT vendors.

For teleradiology, AI usage in image analysis remains relatively limited; most instances of AI adoption to-date have been in relation to improving workflow efficiency. They have predominantly involved teleradiology reading service providers partnering with third-party AI specialists. However, Nines and Braid.Health are some exceptions to this, and instead natively developed AI solutions to strive towards better workflow integration, ultimately offering a market differentiation. Somewhat surprisingly, Nines’ journey was cut short in March 2022 following the announcement that Sirona Medical was acquiring its AI capabilities (two native AI solutions – ICH detection and lung nodule detection – and AI software developers). However, teleradiology AI providers have largely fared well to-date, most notably DeepTek which has achieved impressive growth and has its sights set on international expansion.

Diversification and the Growth in Sub-Specialisation

Reported revenues from outpatient providers in 2022 have shown that many are still feeling the lasting effect of the pandemic and Covid-19 variants. Coupled with the indicators of general economic downturn; rising inflation and the prospect of an impending recession, providers are becoming increasingly risk averse. As a result, providers are increasingly diversifying their product and service portfolio, offering sub-specialisation in areas such as neurology, mammography, and oncology, or advanced imaging services, including PET, MRI, and CT.

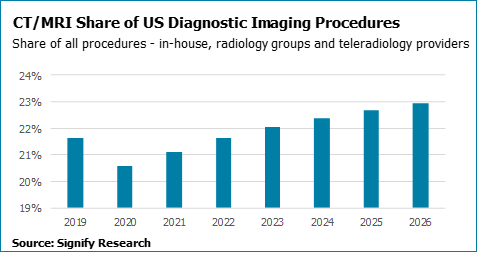

The utilisation of CT and MRI is forecast to grow from 21% share of overall US diagnostic imaging procedures in 2021, to 23% in 2026. In absolute terms, this translates to volume growth of 6% (CAGR), significantly outpacing the growth of other modalities, especially X-ray (+2% CAGR). As demand for specialised modalities increases, so does the requirement for specialist radiologists capable of interpreting more complex examinations. Where access to sub-speciality expertise can be limited in-house (e.g. in smaller hospitals), teleradiologist expertise provides an ideal solution.

As well as outsourcing to teleradiology providers, advanced imaging services evolve a provider’s IT requirements, driving provider investment towards sophisticated imaging IT platforms that can support the customers’ breadth of specialist services, as well as the workflow to management external referrals, such as teleradiology. This will place pressure on smaller imaging IT vendors, exacerbated by larger imaging IT vendors looking to enter and grow in this market. In the medium-term, the expansion of specialism could expose the smaller specialised vendors to acquisition.

Considerations for the Rapidly Growing Market

Coming out of the pandemic, smaller imaging centres found themselves in vulnerable financial positions, leading to M&A activity, already present in the US market pre-pandemic, intensifying. Private equity, hospitals, and larger imaging centre networks all continue to invest and acquire across the US, with many of the larger imaging chains such as RadNet and SimonMed demonstrating aggressive acquisition strategies. As a result, imaging IT contracts are becoming larger, both in value and length, delaying opportunities for vendors to disrupt the competitive landscape.

As outpatient providers consolidate, so will IT contracts. Although not immediately, as IT consolidation typically aligns with contract expirations, it remains a threat to vendors’ installed bases. Specialist integrations, AI tools, cloud-native deployment and, in general, a platform’s key feature differentiators will be increasingly important in winning and maintaining share as the competitive landscape intensifies.

Teleradiology groups are yet to observe the same consolidation trend as traditional outpatient providers, however the accelerated demand for teleradiology services over the past 12 months has posed different challenges, such as ensuring adequate resourcing capacity. A task made tougher by an unprecedented radiologist shortage in the US, driven by burnout and wage inflation. To attract and retain radiologists, teleradiology market leader vRad set the tone 12 months ago by announcing a substantial compensation rise of up to 25%, beginning in January 2022. Increases ranging from between 10-30% have also been common across many US-based teleradiology providers this year.

Whilst teleradiologist wage inflation and subsequent higher reading fees could deter some healthcare providers from outsourcing their diagnostic imaging workload, the reality is that most healthcare providers are in desperate need for external support and view teleradiology as a necessity to ensure efficient reading turnaround times and provide high-quality patient care.

Who’s Ready to Capitalise?

The US market has an increased reliance on outsourcing, for both image acquisition and image reading, as the demand for imaging procedures continues to grow faster than the supply of radiologists. Thus, outpatient providers, including teleradiology groups, offer acute providers accessibility to sub-specialists, alongside the utilisation of technology that drives greater productivity within an organisation. For teleradiology groups, ensuring they have the radiologist capacity and technology in place will be essential to capitalise on the opportunity for robust market growth.

For imaging IT vendors, platform investment must drive workflow optimisation within an increasingly complex and growing network, as well as integration of specialist tools, such as AI, and deployment via the cloud. With no vendor achieving this at scale, it’s an environment that leaves the market open for disruption

About Signify Research

Signify Research is an independent supplier of market intelligence and consultancy to the global healthcare technology industry. Our major coverage areas are Healthcare IT, Medical Imaging and Digital Health. Our clients include technology vendors, healthcare providers and payers, management consultants and investors. Signify Research is headquartered in Cranfield, UK. To find out more: enquiries@signifyresearch.net, T: +44 (0) 1234 436 150, www.signifyresearch.net

More Information

To find out more:

E: enquiries@signifyresearch.net,

T: +44 (0) 1234 436 150