Written by

Share article:

Cranfield, UK, date 31/01/2024 –

Digital breast tomosynthesis market to rise 8.1% from 2022-2027: When will 3D mammography screening be introduced outside of the USA?

2023 stood out as a turning point for the breast imaging market, due to the diminished impact of COVID-19 and a rebalance in market demand. In 2022, breast imaging revenue was down 17.6% compared to 2021 as vendors suffered a shortage of semi-conductors, inflation hikes, and a market correction following elevated investment on breast imaging systems in 2021 as budgets returned post-COVID.

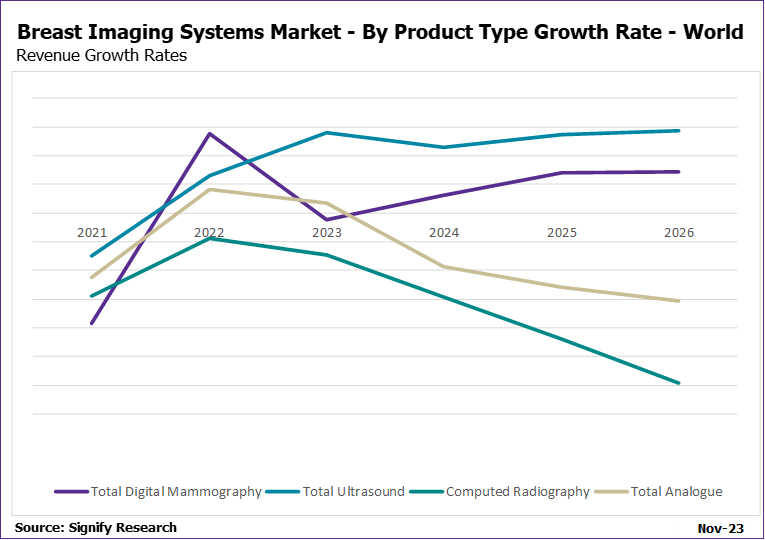

Overall, breast imaging revenue grew 12.5% in 2023 and is forecast to reach $1.18 billion by 2027. This is driven by introduction of novel screening programs, digitalisation within developing countries, and an increasing proportion of digital breast tomosynthesis (DBT) and automated breast ultrasound (ABUS) system purchases.

Currently, DBT accounts for over half of the global breast imaging market’s revenue, fuelled by its high average selling price, and popularity in Western Europe, North America and Oceania. These regions are also actively investing in DBT equipment in preparation of breast cancer screening programmes by transitioning to DBT, as seen in the United States.

This is likely to occur in the mid-term as the TOSYMA and TMIST DBT trial results are expected to be released in 2025 and provide strong evidence for its implementation.

As a result, growth for full-field digital mammography (FFDM) is mostly limited to developing nations. The pricing of DBT is often prohibitive in these regions, making FFDM the predominant solution for the expansion of breast cancer screening and diagnostic capacities. Growth is further fuelled by the replacement of outdated analogue mammography systems with newer digital gantries in regions such as Latin America and Asia Pacific.

The ultrasound market represents a smaller proportion of global breast imaging units but is forecast the fastest annual revenue growth of any breast imaging modality, with an average annual increase of 12.0% over the next five years. This growth is driven by the increase in supplementary screening exams and breast density awareness. The recent change in European guidelines by EUSOBI’s also include the recommendation for supplementary ultrasound when MRI is unavailable which is driving demand further. ABUS is growing at a much faster rate than conventional ultrasound, in China and USA particularly, and with a much higher price point, it contributes heavily to the overall growth of the ultrasound market.

Regional trends:

North America – Overall revenues for breast imaging solutions increased 19.8% in 2023, primarily due to the recovery of supply chains and delayed orders from 2022 being fulfilled. DBT is already used for screening in the USA and in Canada. In Canada, the Society of Breast Imaging recommends DBT in favour of new FFDM systems, which is expected to be implemented for screening applications in the near future.

Meanwhile, breast density notifications will become mandatory in the USA in 2024 and is now required by almost all Canadian provinces. Access to supplementary screening is also increasing in North America as more states and provinces enforce insurance for supplementary screening, spurring growth for secondary imaging modalities.

Latin America – Due to price-sensitivity, Latin America has a large install base for analogue and computed radiography mammography systems. These systems are forecast to decline in favour of digital solutions, making Latin America one of the fastest growing markets for mammography. For ultrasound, there is a lack of trained sonographers making it an underutilised breast imaging modality, despite its low price point.

Western Europe – Despite the region unanimously using 2D mammography in breast cancer screening programs, FFDM systems are declining in favour of DBT gantries. This is due to healthcare providers preparing themselves for an expected transition of breast cancer screening towards DBT. However, this transition is not predicted to occur until after TMIST and TOSMYA trial publications expected in 2025.

Eastern Europe, Middle East and Africa – High growth is projected in the EEMEA sub-region due to increasing investment in women’s health in North Africa and the increasing screening capacity in the Middle East. In Eastern Europe there is also increasing investment in breast imaging solutions financed by EU COVID recovery funds post-COVID. Poland, Greece and Romania were some of the largest recipients, the latter of which will utilise funding for their novel national screening program with a large order of gantries expected to land 2024.

Asia Pacific – APAC lacks formal screening programs and price sensitivity limits the uptake of digital mammography systems here. Ultrasound is heavily relied upon due to its low price point, as well as the increased prevalence of breast density. APAC is forecast the fastest growth in the coming years, due to a largely unaddressed need for mammography screening and the increasing importance placed on women’s health. Much of this growth can be attributed to China’s rapid expansion in breast screening, driven in part by the Government’s ambitious goal to screen 90% of eligible women by 2030.

Developments in the competitive landscape:

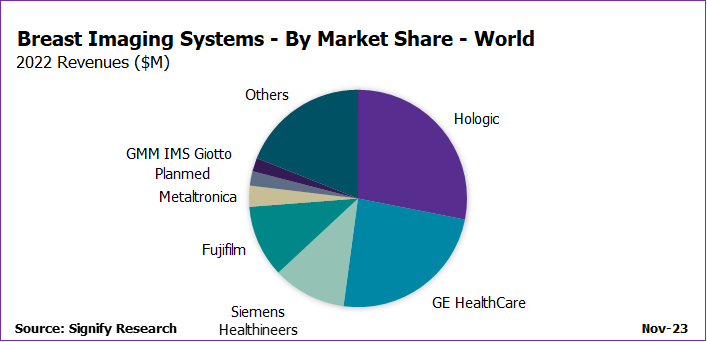

Due to semiconductor shortages market leader Hologic lost single-digit market share in 2022. However, Hologic managed to recoup lost market share in 2023 as supply chains stabilised and lead times returned to normality. 2023 also saw Siemens Healthineers withdraw from the ABUS space, decreasing their overall breast imaging revenue and allowing GE HealthCare to fully capitalize on the increase of supplementary screening in North America.

Fujifilm’s market share is also rising as it focuses on growth within the USA. Its acquisition of Hitachi has also positioned it well in the Breast Imaging market. This acquisition allows them to offer multimodal deals, while their competitive pricing strategy has helped them to win tenders in developing economies as well as securing over 40 DBT systems in the 2023 Italian CONSIP tender.

Breast Imaging AI outlook:

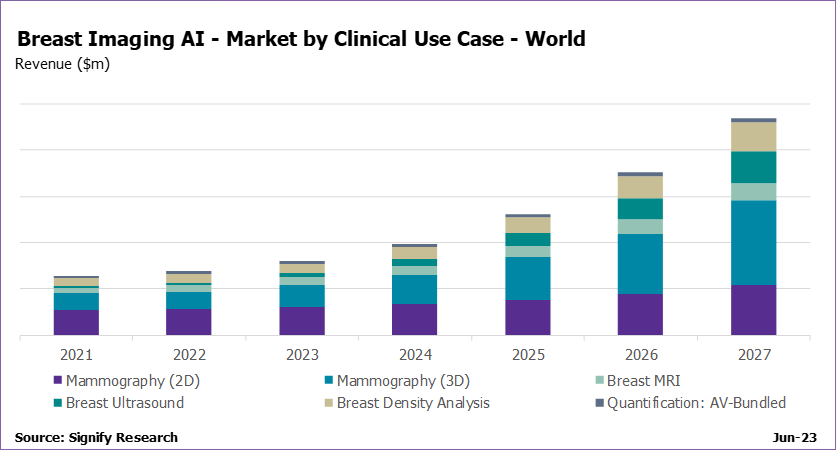

2023 was an exceptional year for developments in breast imaging AI, most notably with the release of ScreenTrustCAD and MASAI trial results, which gave critical evidence for AI’s adoption into screening programmes. They provided largescale prospective evidence for ScreenPoint’s Transpara and Lunit’s INSIGHT MMG non-inferiority when replacing the second reader in breast cancer screening, the standard of care across Europe. Lunit is also now set to begin implementing INSIGHT MMG within the PACS for BreastScreen NSW, the breast screening program for New South Wales, Australia. Success in this phase is expected to secure a 5-year contract with BreastScreen NSW and may lead to Lunit having the first AI to be used in a national screening program, if Australia seeks to expand the initiative.

The global Breast Imaging AI market is predicted to reach $233.9 million by 2027 with Americas accounting for over two thirds of the market. DBT AI will account for much of this growth due to its promise in reducing their extended scan times compared to FFDM and the pending implementation for DBT in screening outside of the USA. Currently however, 2D accounts for most breast imaging AI solutions on the market as 2D images are still the standard for mammography until DBT is approved for screening elsewhere.

Final Thoughts:

The Breast Imaging market is predicted to experience growth in DBT systems, while the demand for FFDM systems is expected to decline in mature markets. Globally, the FFDM market is predicted to see a modest growth driven by digitalisation of developing countries, the introduction of novel screening programmes, and increased breast cancer awareness.

The global breast imaging market is predicted to remain flat in 2024, with DBT and ultrasound leading the 5-year forecast in terms of revenue growth. Supplementary screening modalities, such as GE HealthCare with their Invenia ABUS system, will provide increasing returns, as legislation supporting supplementary screening increases. Contrast-enhanced mammography capabilities are also likely to become an industry standard for gantries, given their quicker acquisition and interpretation by radiologists compared to MRI scans, which are often prioritised for other exams and therefore unavailable for breast imaging.

In developing markets, system pricing and cost of ownership is a key determinant for decision making as healthcare budgets are continually threatened by inflationary pressures. Vendors offering competitive prices, such as Fujifilm, are expected to achieve considerable success, especially in winning tenders, ultimately leading to lucrative service contracts to provide consistent returns on systems.

Related Research

Breast Imaging – World – 2023

About The Author

Having graduated from the University of Bristol with a BSc in Pharmacology, Max joined the Medical Imaging team at Signify Research in 2023, focusing on the X-ray market.

About the Medical Imaging Team

Signify Research’s Medical Imaging team formulates expert market intelligence for some of the leading Ultrasound, CT, MRI, and X-ray vendors. Combining primary data collection and in-depth discussions with industry stakeholders, our thorough research approach yields credible quantitative and qualitative analysis, helping our customers make critical business decisions with confidence. Furthermore, our commitment to seeking a plurality of perspectives across the markets we cover guarantees that our insights remain independent and balanced.

About Signify Research

Signify Research provides healthtech market intelligence powered by data that you can trust. We blend insights collected from in-depth interviews with technology vendors and healthcare professionals with sales data reported to us by leading vendors to provide a complete and balanced view of the market trends. Our coverage areas are Medical Imaging, Clinical Care, Digital Health, Diagnostic and Lifesciences and Healthcare IT.

Clients worldwide rely on direct access to our expert Analysts for their opinions on the latest market trends and developments. Our market analysis reports and subscriptions provide data-driven insights which business leaders use to guide strategic decisions. We also offer custom research services for clients who need information that can’t be obtained from our off-the-shelf research products or who require market intelligence tailored to their specific needs.

More Information

To find out more:

E: enquiries@signifyresearch.net

T: +44 (0) 1234 986111

www.signifyresearch.net