Share article:

Helsinki, Finland | July 2019 | Michael Liberty – The HIMSS & Health 2.0 European Conference attracted over 2,600 delegates from 64 countries to Helsinki in June 2019. While there was a strong focus on healthcare in the Nordics, the conference brought with it a wide variety of vendors from across the globe all looking for new opportunities on the show floor. Our key takeaway – the goal to change mindsets in Europe towards how healthcare can be improved through the use of technology. We look at a few examples below, namely:

- Developing Integrated Care Networks Through Regional Procurement

- Better Localisation of EMRs

- The use of Telehealth

Regionalisation Becoming the Norm

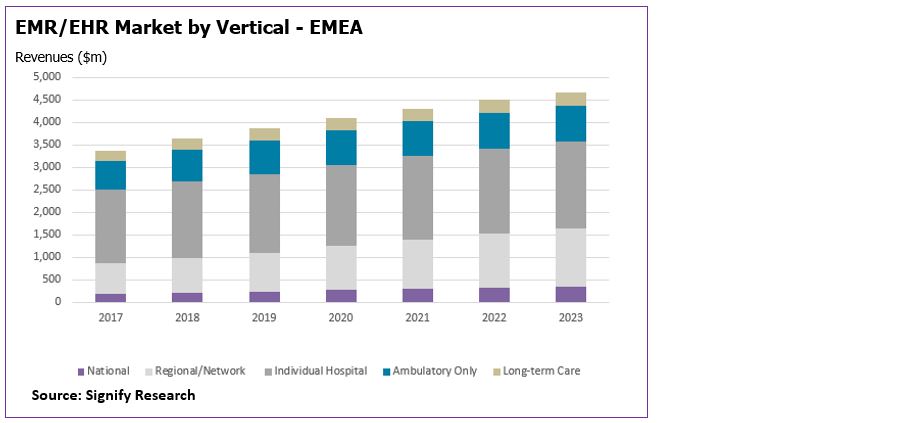

The push towards implementing new innovative healthcare models is gaining momentum across Europe, with a few examples showcased on the agenda at HIMSS. Vendors looking to operate in this market are increasingly having to work with complex regional health systems and interoperability frameworks. The below figure shows projections for the EHR market in EMEA, with splits for type of solutions purchased. It shows Regional/Network EHR spending is forecast to grow at the highest rate over the next four years, starting to rival the market for EHRs purchased by individual hospitals by 2023.

All of Estonia’s health data is effectively digitised, including prescriptions and billing, while also incorporating blockchain technology, all while using local digital vendors. The next step for Estonia is to move towards preventative services for breast cancer and cardiovascular diseases, with a goal to create individual health plans for citizens by 2023.

The Dutch government also came out in force at HIMSS with Nictiz, the MoH independent interoperability group, outlining its goals to deliver information exchange. Its core goals are to standardise medication data by 2019, create a patient accessible EHR by 2020, create a unified national data exchange network and to deliver longitudinal records at the point of care. A lot of the discussion was around scaling these solutions at a regional and national level, but also including major stakeholders from providers and vendors to get organisations onboard early. This could open up opportunities to work closer with these larger regional organisations for Netherlands’ HIS vendors Chipsoft, Cerner, Nexus and Epic.

The Need for Localisation

Historically, there have been two major points of entry for international EMR vendors to penetrate into a new geography; either through a partnership to gain expertise and ‘localise’ a solution or through acquisition of a local vendor. Both have their challenges, with acquisition often resulting in the long-term support of a legacy solution (e.g. Cerner is still supporting several legacy Siemens EMR solutions nearly five years after announcing its acquisition plans) and partnerships often being slow. Examples where vendors have taken on large regional projects before ‘localising’ solutions, have often resulted in projects running over budget and negatively affecting both vendors and providers alike.

One vendor with growing stakes in the Nordic markets is Epic, and HIMSS Europe provided a chance to hear some key learnings from its three major EpicCare implementations at different stages across the region. Each is sold under the idea a large regional project needs a scalable solution which can deliver interoperability and future functionality around integrated care or PHM. In Finland, it is underway implementing its integrated social care record (including Epic’s HealthyPlanet) across four municipalities, although this has already been hampered by some delays.

During the Accenture Workshop, we got a chance to hear from both the upcoming Epic deployment in the Norway Central Region and the learnings from the Capital Region deployment in Denmark from the implementation teams at the heart or the projects. In both cases, the governments went against contracting with the local vendor (Systematic in Denmark, DIPS in Norway) and looked towards regional teams to implement the Epic solution.

Issues around the Danish implementation were exacerbated as it was Epic’s first deployment in the country. This complicated medical translations from its US EHR, adding to the idea some form of localisation prior to winning a large regional project would have eased some of these issues. A key discussion point around the deployment in Denmark was the resistance put up by EHR users on the go-live date. A lack of engagement with clinicians to understand the nuances of their existing workflows resulted in backlash when the new system required additional input on their end.

This is something which arguably should have been core to the project plan from the start for both the providers and the vendors side. The Norwegian Central Region should look to engage key stakeholders in its upcoming deployment, as well as outlining how to measure success post its roll-out.

This pivots into what was my key takeaway from HIMSS Europe. There are far too many examples on the global market of vendors over promising what they can deliver without fully understanding all the nuances in a country’s healthcare ecosystem. While many solutions are procured at a hospital or regional level, the ones using solutions are the clinicians and physicians and they will ultimately have a major influence in whether a deployment has been successful or not.

This group’s importance is seemingly underestimated and engaging this group at an early stage can be invaluable to making sure health IT is being used effectively and delivers on its initial goals. The onus of a delayed or overbudget delivery will fall on a vendor’s shoulders and poor implementation can have ramifications for the future rollout of health IT in a given country.

Scaling Virtual Care

From on-demand video consultations, to the deployment of tele-stroke networks and the plethora of remote patient monitoring programs underway, it seems that Europe is finally starting to catch up on the US in terms of telehealth, and at last is moving beyond the pilot/trial status that has defined the market for many years. This move from pilot to scaled deployment was evident on the show floor at HIMSS Europe.

Primary Care

Consumer on-demand video consultations are now widely deployed in the US, with companies such as American Well, Teladoc, MDLive and Doctor on Demand, providing several million low-acuity consultations on behalf of commercial payers and employers every year. The structure of many European primary care markets, with local independent GP practices providing government-funded primary care, has meant market entry for commercial telehealth service providers has been complicated. The incentives for local providers to develop telehealth services of their own has been lacking. However, this is starting to change and at Helsinki several local virtual care platform and service providers showed numerous cases of local successes setting the scene for scaling their success across the continent.

LIVI or KRY (as it’s known in Sweden) was demoing its virtual care services on the floor in Helsinki. The company initially had success in the telehealth market providing low-acuity video consultation services in Region J√∂nk√∂ping, Sweden. It started offering these services in 2015 and by the end of 1Q19 had provided more than 700,000 virtual consultations. At the show it was pushing its geographic expansion credentials, specifically those in France and the UK with plans to move into Germany later this year. It tackles geographic expansion by partnering with local providers or setting up its own local primary care networks and using its virtual care platform to direct patients to its clinics. It is estimated to have raised over 79M through Series A and B funding, with its major customers being families on a pay-per-consultation basis. In the UK it is already active across Northampton and North West Surrey GP practices. However, its forays into France suffered a setback, with government reimbursement decisions not going its way, potentially limiting the company’s medium-term success in France. This is not just an issue in France, and as telehealth service providers expand their geographic footprint, ensuring they can navigate local reimbursement structures will be key to success.

VideoVisit was another Nordic telehealth solution provider showcasing its offerings at HIMSS. VideoVisit is slightly different to KRY in that it is a platform provider and not involved in directly providing healthcare services, i.e. it provides the tools to allow bricks and mortar primary care physicians to roll out their own telehealth services. Where it does have similarities is it is also looking to provide a solution for patient-to-provider home video consultations. However, it has started to address other parts of the telehealth market, such as provider-to-provider consultations and supporting higher-acuity patients with chronic conditions. It was in this area that is was pushing its new products at HIMSS Europe, namely VideoVisit REMOTE. VideoVisit REMOTE is the product of a joint venture with Taiwan-based Medimaging Integrated Solutions (MiiS) and is focused on supporting remote diagnostics. VideoVisit is Finland’s largest telehealth vendor, mostly known for selling its outreach solutions sold directly to the Finish municipalities. With little local competition, its goals are to expand its telehealth offerings in Finland and scale its services internationally, with it securing ‚Ǩ1.5M funding in May 2019.

Inpatient Care

The above focused on the use of telehealth in non-emergent settings. However, demand for technology to support telehealth in acute and inpatient settings is also growing in EMEA. The EMEA market for telehealth platforms, hardware and services in acute settings is forecast to be worth more than $500M in 2022 (according to Signify Research’s 2018 telehealth report). However, this is still much smaller than the equivalent North American market forecast (>$900M). That said several vendors that have generated significant revenues in the US acute market, were at HIMSS Europe in an effort in tap into broader international markets.

Philips was one, demoing its TeleICU technology with its major strategy in Europe aimed at working with central hospitals with larger ICU departments. The overwhelming majority of Philips’ TeleICU business is driven by the US; however, it has also had success in selling its solution in the UAE, India, the UK and Japan. It’s one of the few vendors in the marketplace to offer a centralised solution. However, this does present some challenges in relation to the cost of the technology and cost of process reengineering when being implemented. For this reason, the number of Philips TeleICU customers in Europe has remained relatively low to-date. However, Philips has proven the business model well in the US market where approaching 20% of all ICU beds are monitored using TeleICU technology. As hospitals in Europe are increasingly digitised, the market for TeleICU solutions is forecast to start to ramp up and Philips is positioning itself well to take advantage of this.

GlobalMed was another example of an inpatient telehealth solution vendor that is largely driven by US, inpatient business, that was at HIMSS Europe to push its international credentials. The company already does have good credentials in terms of EMEA business with success in UK, Spain/Portugal, Slovenia, the Middle East and Africa, providing solutions for inpatient surgical and medical support. Its recent announcement to implement its virtual care platform on Microsoft Azure, restructure some of its cart and platform packages to SaaS-type models and beef up its EMEA team will certainly support its continued international expansion.

Whilst the primary care telehealth market is defined by vendor/service provider fragmentation, the acute/inpatient market is markedly more consolidated, with vendors such as the two above, along with US-based InTouch Health, Avizia (now owned by American Well) and AMD Global dominating the market. None of these others were at HIMSS Europe this time, but like above, their presence in 2020 would not be a surprise.

About Signify Research

Signify Research is an independent supplier of market intelligence and consultancy to the global healthcare technology industry. Our major coverage areas are Healthcare IT, Medical Imaging and Digital Health. Our clients include technology vendors, healthcare providers and payers, management consultants and investors. Signify Research is headquartered in Cranfield, UK.

About the Author

Michael has 5 years’ experience as a Senior Market Analyst, working across multiple industries and specialising in developing forecasting models and database management. Michael joined the Signify Research digital health team in 2018 and currently leads our PHM coverage, as well as specialising in the EMR/EHR and RCM markets.