Written by

Share article:

Cranfield, UK – 17th October 2019 – The growing influence and uptake of electronic medical records (EMRs) in healthcare has driven debate over the future role of specialist clinical and diagnostics software. With interoperability in the health sector still a major challenge, many health providers are looking to simplify their IT systems, consolidating to fewer software platforms and few vendor partners. With recent extensive and long-term investment in EMR systems, some healthcare providers considering the EMR as a potential candidate to extend into diagnostic imaging. In this summary we identify the challenges with this approach and discuss why we believe dedicated imaging IT software is a long way from being replaced by EMRs.

Complexity

Radiology is often viewed by hospital leadership as a singular entity. It is really a collection of a sub-specialist systems, each with its own unique requirements. At a large acute-care hospital, there are dozens of different imaging modalities in operation (usually from a selection of different vendors), conducting thousands of different scan types, round the clock. These images must then capture and routed, processed, analysed, annotated, reported on, archived and exchanged.

Unlike much of healthcare, radiology has been digitasing for over 30 years; radiology IT software that is available today from market leaders is the product of decades of experience. For example, seamlessly integrating digital tomosynthesis breast scans (comprising many hundreds of images) into conventional radiologist reporting workflow is not easy; it requires specialist software. The number of images, size of the study (most are ~200MB compressed), requirement to be able to review different planes and necessity for the radiologist to “slab” images, thereby consolidating some images together, as well as share studies or even report remotely, makes it a big challenge from a technical standpoint. Add-in specialist reporting and registry requirements for breast imaging, the growing use of additional AI-based quantification or decision support tools and the need to include other modality images (such as conventional 2D mammography, automated breast ultrasound (ABUS) and MRI) and the complexity is clear.

Few, if any, EMR systems today can support multi-modality breast imaging in their core clinical module offerings; unsurprising perhaps give that may of the world’s top imaging IT vendors are also still grappling with the challenges of DBT for breast imaging. But this is just one example of the myriad challenges posed by modern radiology – each sub-speciality (abdominal, breast, cardiac, emergency medicine, musculoskeletal, neurology, paediatric, thoracic, vascular etc.) in radiology has a unique and specialist blend of imaging types, user requirements and diagnostic tools. Amassing these into a single coherent software platform has taken leading vendors decades and billions in investment.

Cannibalisation of RIS has driven new wave of specialist demand

While this complexity is inherently “baked-in” to radiology, there are some functions and areas of radiology IT software that have become more commoditised. For example, imaging order-entry and basic workflow scheduling for imaging modalities, long the mainstay of specialist RIS systems, have often been replaced in favour of an EMR vendor RIS module. Most EMR RIS’ have solid functionality in handling the basic operational processes for a radiology department and enabling enterprise-wide access and diagnostic report – patient record integration. Cannibalisation of standalone RIS systems by EMR vendors has been relatively widespread over the last decade, especially in the US where the confluence of regulatory enforcement and market economics resulted in mass hospital M&A activity into larger networks. Consequently, the standalone specialist RIS market declined year on year.

Yet this shift has not had the desired effect expected by commissioning hospital executives. In fact, the reactionary impact of this decision to use EMR over specialist RIS has been quite profound. Many of the nuanced tools and features of standalone RIS were missed by radiologists and technicians; speciality functions such as modality protocol management, smart enterprise case-load balancing, staff QA, fleet management servicing and so on were all missing from EMR RIS offerings. Moreover, with more access to operational data from the EMR roll-out, hospital leaders are today realising that imaging has a major role in care operations, as both a profit and loss centre. And it has even more of a bearing on clinical outcomes.

The result of this cannibalisation? A new wave of specialist standalone workflow and operational products for radiology has emerged, with a clear migration of radiologist workflow tools from RIS products towards radiology PACS, which in general has been far less impacted by the EMR. Leading imaging IT vendors have also been quick to jump on this trend, especially as focus on operational efficiency, cost saving, and care outcomes have become more important in today’s regulatory environment. The sudden acquisition spree of specialist workflow software vendors such as Primordial (Nuance), Medicalis (Siemens Healthineers) and Clario (Intelerad) and product launches of workflow, operational and business intelligence tools from leading vendors, is spurring robust new market demand (see chart); this can only reinforce the argument that EMR-based RIS has so far not been able to meet the complex needs of radiology.

Enterprise Imaging Strategy Still Emerging

For some hospital executives, given the long-term investment and dominance of the EMR, there may also seem to be few coherent alternatives to the timely extension of EMR into the diagnostic sector. This is in part due to the relatively slow movement of the imaging IT industry. Radiology IT has traditionally been based on PACS/RIS, essentially single department image management and archive software. Today, most of the global installed base is still standalone.

Yet imaging IT has been evolving a lot in recent years. New imaging IT software has evolved to focus on centralising core imaging and diagnostic reporting across the enterprise, bringing other allied disparate imaging or diagnostic applications into a single platform. The net result of this is intended to support health providers pursue an “enterprise imaging” strategy, consolidating all types of imaging software together.

The industry has though done a poor job of explaining the concept of enterprise imaging as a strategy, as opposed to a product. Many have also used “enterprise imaging” to describe “enterprise radiology”, connecting disparate PACS in multi-site networks. While a clear benefit as a short-term solution to combining core radiology at scale, this approach has missed the operational and clinical value of consolidating unstructured imaging and clinical data other diagnostic departments (dermatology, emergency medicine, surgery, gastroenterology, etc.) into a centralised imaging platform.

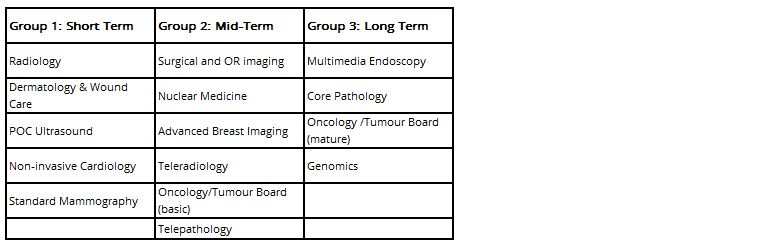

Positively, the “enterprise imaging” strategy is slowly gaining traction, with recent major deals showcasing the combination of radiology with other disciplines. In our earlier piece following the SIIM2019 show we also identified in which other diagnostic disciplines imaging IT platforms were having most impact and how quickly. These are outlined below:

The consolidatory effect of an enterprise imaging strategy can be important, both from a financial and care-outcome perspective.

For example, bringing together imaging from radiology, surgery and pathology into a common platform, interfaced with the EMR and dedicated oncology IT, is showing clear benefits for care outcomes; these are commonly known as multidisciplinary “Tumour Boards”. Integration of unstructured data from dermatology (visible light images) or point of care ultrasound (POCUS) also supports healthcare providers in filling in gaps of patient medical records (often these scans or images are not scheduled, or archived centrally); this offers both clinical benefit, as well as financial gain in terms of missed billing opportunities.

However, there are still relatively few case studies of mature enterprise imaging at scale in the market, though the list is growing. Multi ‘ology mature enterprise imaging is a long-term and complex strategy to implement; consequently, few healthcare providers have “completed” it, with most still in the early foundational stages.

With a relatively small body of evidence as to its effectiveness, this makes it harder for health leadership to take the concept of enterprise imaging seriously against the backdrop of EMR expansion and growing leverage in decision making.

EMR and Mature Enterprise Imaging Can Co-Exist

Perhaps most importantly, there may need to be a change in thinking at the executive level of healthcare providers.

In the case of radiology specifically, market evidence suggests that EMRs have some way to go if they are to fully replace standalone radiology IT. Instead, health providers should be looking for where the scale and breadth of the EMR can be augmented by the depth and specialism of radiology IT and vice versa.

For example, enriching core radiology software and the user interface with curated longitudinal patient data from the EMR is viewed as a positive way to improve the quality of diagnosis. At the same time, implementing advanced image archiving and clinical data management, usually an outcome of mature VNA implementation most commonly driven by radiology, can lay the foundation for management of imaging and other data outside the EMR.

Perhaps most potential for improvement in care-co-ordination and broader diagnostic data management lies not in replacement of the radiology IT, but in supporting its evolution to enterprise imaging. Putting this is place for many health providers is clearly a daunting task; however, solutions to support interplay between systems are increasingly available and are becoming part of imaging IT vendor portfolios.

Health providers should also consider auditing their vendor partnerships when it comes to radiology IT; they should look beyond just a point solution for radiology and consider the capability of their vendor to support an enterprise imaging strategy and in the context of their existing EMR framework.

In addition, this central vendor partner should also support their navigation and building the foundation for managing imaging and associated diagnostic content across the enterprise. This has many benefits, both in terms of reducing the number of unstructured imaging data generating applications, simplifying supply chains, reducing the need to manage and secure a patchwork of ageing modules, or by acting as a “curator” for specialist best-of-breed functionality. The latter is also increasingly important as radiology and other diagnostic departments move towards using AI; with hundreds of new tools and products entering the market, a central imaging IT vendor should act as a contractor for its customers in implementation.

In conclusion, each health provider will judge the potential of EMR and specialist imaging IT against its own specialist and unique criteria. What is clear is that no EMR vendor can today handle the complexity and specialty requirements of modern radiology within its EMR offering, nor should it try. Instead, health providers should be looking for a central diagnostic imaging IT specialist that can support it in embracing an enterprise imaging strategy.

Related Market Report

“Imaging IT Market Intelligence Service 2019“. This Market Intelligence Service is an annual subscription that provides ongoing data, insights and analysis on the global opportunity for Imaging IT.

About Signify Research

Signify Research is an independent supplier of market intelligence and consultancy to the global healthcare technology industry. Our major coverage areas are Healthcare IT, Medical Imaging and Digital Health. Our clients include technology vendors, healthcare providers and payers, management consultants and investors. Signify Research is headquartered in Cranfield, UK.