Written by

Share article:

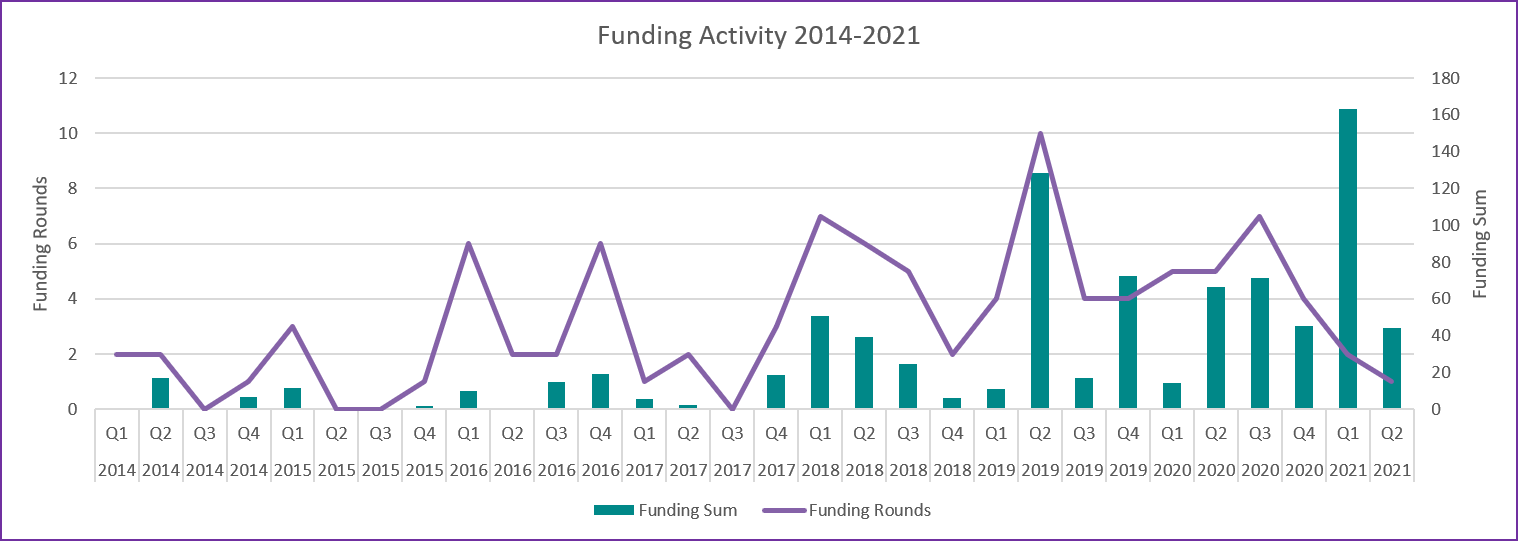

14th April 2021 – Written by Imogen Fitt – Investment for companies developing digital pathology solutions has totalled more than $860 million since 2014. Despite the COVID-19 global pandemic, almost a quarter of the total funding ($207.0M) has been raised so far this year (2021). Investment is now evolving to focus on start-ups developing AI solutions for digital pathology image analysis.

UPDATE: We have since released an update to this analysis. Click to here to be redirected and find a new updated download.

This report covers:

- The total funding and number of deals by quarter since 2014.

- The type of investments raised by companies since 2014.

- The distribution of funding regionally and by company.

- The number of recently funded digital pathology companies by founding date.

- The topmost funded companies.

- The total investment vendor type (target market, product type).

Funding for digital pathology companies has reached over $860M since 2014, with 73.4% raised since 2019. Investments have begun to increase in size as recent challenges faced by global healthcare providers have highlighted the need for pathology departments to digitise, with almost a quarter of the total funding ($207.0M) coming early this year (2021).

Whilst 68.8% of funding raised was dedicated to US-based companies, investment is also beginning to scale in other international markets as companies mature and seek later stage funding.

Compared to the beginning of the decade, there has been a notable shift in investment from hardware/software solutions towards AI-image analysis. The three largest unique vendor deals noted in the period include Paige.AI ($125M Series C), PathAI ($60M Series B, and Volastra ($44M Seed). It has also been noted that those companies seeking to focus and specialise in the preclinical market (like Volastra and Owkin) often receive larger funding amounts at an earlier stage, likely due to the higher potential ROI for vendors entitled to drug royalties and lower regulatory barriers for adoption.

Summary of the Key Findings:

- Whilst 2014-2017 reflected a relatively quiet period for investment in digital pathology, over the last three years there has been a significant uptick in funding. This is mostly for software vendors focusing on AI, reflecting a growing confidence in the market’s potential.

- Vendors targeting the preclinical market have experienced higher levels of funding at an earlier stage compared to clinical counterparts. This is likely due to the higher potential ROI for vendors entitled to drug royalties and lower regulatory barriers for adoption.

- Relative to markets like medical imaging AI and AI in drug development, investment in DP remains modest. Penetration of digital pathology remains low, in part due to regulation, the fragmented supply chain and limited investment from healthcare providers in modernising clinical labs so far.

This research relates directly to our upcoming study ‘Digital Pathology – World Market 2021‘. If you would like to know more about our services, or would be interested in engaging with us in our ongoing research, please contact Imogen.Fitt@signifyresearch.net

For a full in depth look at these trends and more please click here to download the latest report brochure.