Share article:

Healthcare IT is becoming increasingly complex. In order to keep up with current and future requirements, Advanced Visualisation vendors are organising themselves into two different categories, each specialising to try and stay ahead of competition. ECR this year offered a glimpse of this growing split; some vendors are focusing on interoperability and integration to become preferred platform vendors, while others are aiming to provide superior image analysis and visualisation software to create the AV tools radiologists would desire and demand. What used to be one complete AV solution from one vendor, may soon become two separate products with companies working together in partnerships to offer a pick and choose selection from the leading AV tools vendors.

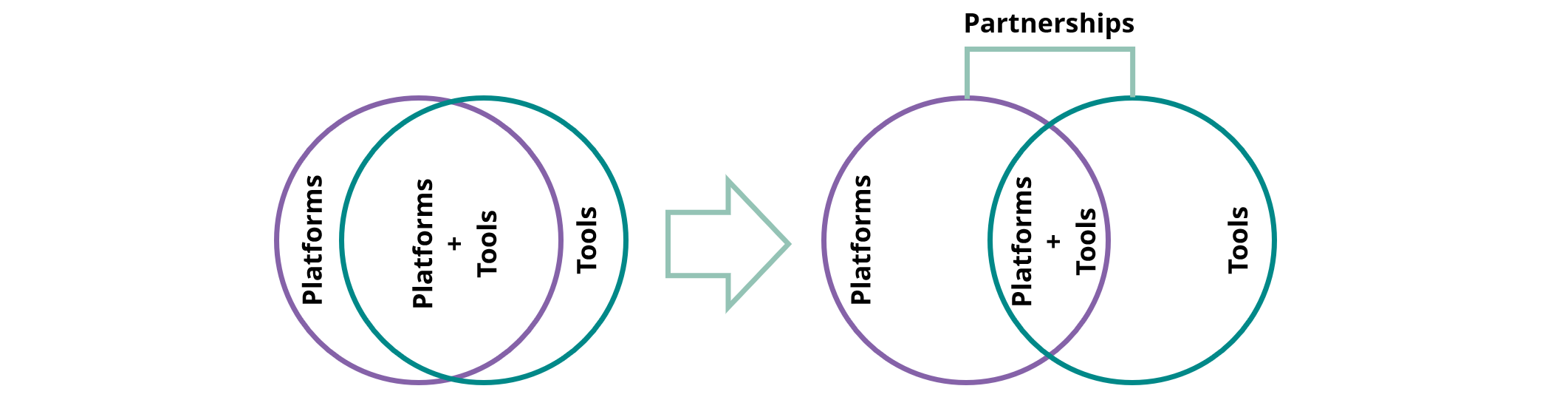

Why is AV Breaking in Two?

A significant proportion of healthcare providers are moving away from the standalone PACS and workstation setup with a separate and isolated system used by the radiologists or technologists only, and towards an enterprise-wide imaging solution, which over time could enable EMR integration, business analytics, genomic data integration, and AI workflow and analysis tools. This integration with the wider healthcare IT requires specialisation and a single point of contact for consultative implementation and customisation. Most AV vendors do not have the capabilities or wish to take on these additional tasks, unless they also have sizeable PACS and enterprise imaging businesses, and instead focus on their core strength; providing image intelligence for diagnostics.

When it comes to image analysis, tools are becoming increasingly sophisticated and specialised into all the different applications, functions and tissues. AV tools are increasingly getting automatic segmentation and measurements integrated into heart, lung and neurology applications, AI for detection of disease-related biomarkers, and AI brain volumetric analysis for neurodegenerative diseases. The prospects of virtual and mixed reality for interventional radiology, cardiology and oncology adds another layer of complexity when it comes to functionalities and integration with current viewing solutions.

The widening of clinical demand for AV, together with the increased integration requirements for platforms, has therefore made it harder to have a complete solution and enter the market independently. Consequently, companies increasingly focus on either providing the best platform or the best individual tools, and enter partnerships to get AV tools to the market or improve the clinical capabilities of an AV platform.

Risk of Being Caught in the Middle

When it comes to “owning” the platform space, the big modality vendors have an obvious advantage since an AV platform is often provided as part of the modality deal, such as CT or MRI. This means it will be very hard for competitor AV specialists to sell an alternative platform to the provider. Moreover, enterprise PACS has also proliferated, adding further consideration in terms of integration across a broader clinical reach. AV vendors continuing to offer their products as a “platform+tools” package therefore have substantial barriers to entry due to brand loyalty and high migration costs, as the provider is often using a platform from their modality or PACS vendor. Although the challenging specialist AV tools may be superior, the provider may not wish to give up the existing platform and user interface, and the deal falls through. A potential sale of a superior AV tool could therefore easily be unsuccessful, if it is tied to a platform which the provider doesn’t need, or if the specialist tools being offered do not easily integrate into the incumbent platform.

How to Succeed as an AV Platform Vendor or AV Tool Vendor

With the industry breaking in two, one needs to not only determine what the core capabilities of the company are with regards to diagnostic tools and platform development, but to also consider the current platform installed base. Should you be a modality vendor with a large AV platform market share, and the capacity to over time develop a fully integrated system with AI workflow, analytics and pre-analysis tools, EHR and genomic data integration, then owning the platform space will provide long-term market success. However, sustained focus on seamless integration of data and software for the continuum of care, provider management and PHM is essential to this strategy. To obtain seamless integration of AV tools, a framework should be established for AV tool partners to streamline user interface and functionalities.

For vendors with core capabilities in developing diagnostic image analysis tools, partnerships with platform vendors for getting your tools to market will be critical. In order to win in this space, focus on creating the best diagnostic tools on the market, encourage pull strategy by letting your tools be known to the providers and radiologists, develop your tools in a modular way to easily fit with different platforms from the main platform vendors, and partner with platform vendors early in development for customising directly into their platform framework.

Traditional AV vendors with AV platform and tools, but no modalities, need to demonstrate a clearly superior product compared to the modality and platform vendors. Adding a high number of tools like the big modality vendors may not be enough. To avoid being caught in the middle, vendors will need something that appeals to both the clinical and the financial buying drivers of the healthcare provider; a differentiated product with superior integration, intuitive and sleek user interface, simplicity and automation for improved efficiency to reduce healthcare costs. And even then, it might require exceptional commercial ingenuity and marketing skills to make it profitable.

Market Breakup Will Bring Competitors Closer Together

So, will the division between tools and platforms continue to grow? It most likely will. Competitors are increasingly working together in partnerships to provide the best solution for the healthcare provider, offering individual tools on a competitor platform despite having a platform of their own. Startups are getting their tools to the market through partnerships without intending to build a complete portfolio or platform, but solely because they specialise in providing a superior tool that can be easily integrated into other platforms on PACS or enterprise solutions. We may therefore start to see the ecosystem of clinical specialist apps developing in a systematic way, starting with a pre-set framework and interface for each platform, and accessed by the healthcare provider via the main platform from another vendor. This will also apply not only for smaller startups, but also for larger AV vendors wishing to get their tools to market in new geographic regions, especially those undergoing strong provider and competitive consolidation.

Related Market Report

“Advanced Visualisation and Viewing IT – World – 2017” provides a highly detailed, data-centric analysis of the world market for Advanced Visualisation and Viewing IT. Key features include market size estimates, annual growth rate forecasts for 2017 to 2021 and vendor market share analysis.

About Signify Research

Signify Research is an independent supplier of market intelligence and consultancy to the global healthcare technology industry. Our major coverage areas are Healthcare IT, Medical Imaging and Digital Health. Our clients include technology vendors, healthcare providers and payers, management consultants and investors. Signify Research is headquartered in Cranfield, UK.

About The Author

Dr. Ulrik Kristensen is a Senior Market Analyst at Signify Research, a health tech, market-intelligence firm based in Cranfield, UK. He can be reached at ulrik.kristensen@signifyresearch.net.

More Information

To find out more:

E: ulrik.kristensen@signifyresearch.net

T: +44 (0) 1234 436 150

www.signifyresearch.net