Written by

Share article:

The concept of an enterprise imaging strategy was coined over a decade ago, however, it’s only in recent years that the expansion beyond “enterprise radiology” has truly begun. The total market for IT across those nine specialities included in Signify Research’s report reached $6.6 billion in 2022; however, only 20% of market revenue was associated to enterprise deals. When digging deeper into which specialities led the enterprise trend, radiology represented 71% of the total enterprise imaging IT market.

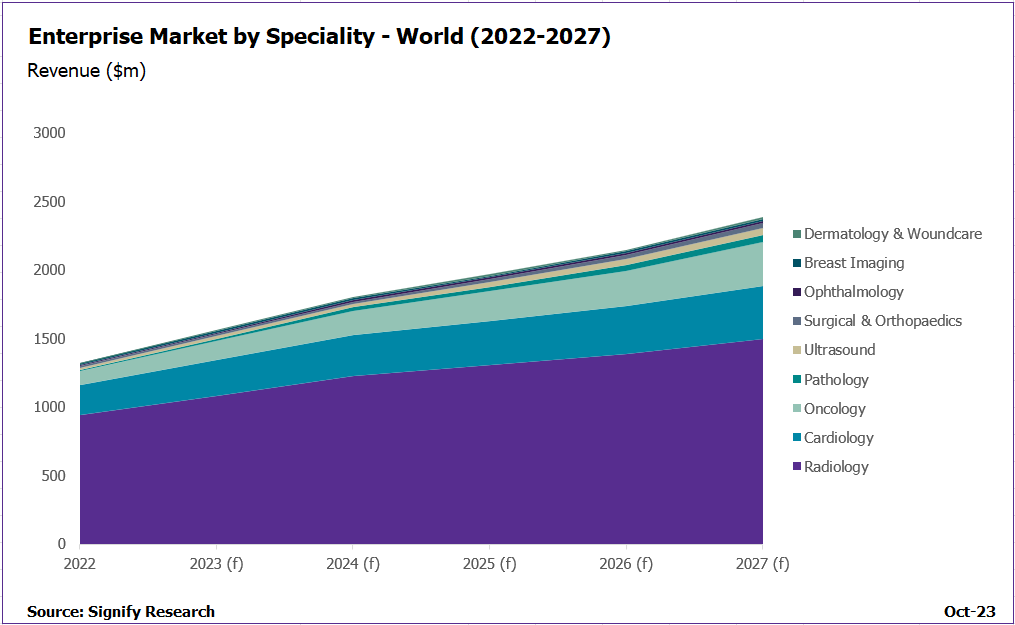

As demonstrated in the graph below, radiology and cardiology are expected to continue dominating the market opportunities for enterprise imaging, representing 79% of enterprise revenue in 2027. Pathology, oncology, and ultrasound IT are the next largest enterprise imaging markets, forecast to represent 18% of the enterprise market opportunity in 2027.

This graph represents the global market revenue from each of these specialities associated to enterprise imaging deals, as opposed to standalone deals. (f) denotes forecast data. This data is taken from our Market Opportunities of Enterprise Imaging – 2023 report, published October 2023.

Recent research with industry stakeholders has centred on the need to consolidate data, make imaging IT systems more interoperable and emphasised the importance of enterprise collaboration to drive better patient care. The question for the market then becomes how do providers and vendors alike move beyond radiology and achieve the ambition of enterprise imaging? And importantly, for imaging IT vendors investment, evaluating what is the true market opportunity?

The Resurgence of the VNA

To take advantage of the momentum surrounding enterprise imaging, most radiology IT vendors are evaluating strategies to leverage existing installed bases to expand into larger, multi-speciality deals. In many instances, that has been a successful strategy, so far. As a result of radiology deals transitioning from standalone to enterprise bundling, stakeholders have evolved. Decisions are increasingly led by C-Suite executives, with the overall influence of the radiology department slowly eroding, limiting some radiology IT vendors from taking advantage of legacy brand recognition.

The success a vendor holds in radiology will however only get them so far, radiology IT vendors will need to evolve along with the market, striving towards an interoperable and optimised platforms for technologies such as cloud and AI. In addition, vendors will need to prove capability in managing imaging beyond radiology and DICOM critical. Expansion into other specialities can be complex, with important considerations on data standards and formats (DICOM, video formats, JPEG, plus other clinical formats that are non-DICOM). In addition to image formats, there are also considerations on the management of encounter-based workflows versus the order-based workflows. Thus, expansion beyond radiology will be inevitably tied to the diversification of the core enterprise imaging platform, often considered the vendor neutral archive (VNA) or equivalent products such as enterprise content management.

Building on the central repository of imaging data offered by the VNA, vendors can begin to differentiate further by leveraging the data, alongside EMR and other sources, to produce actionable insights and analytics, and improve productivity not only in radiology, but across all imaging departments and the overall enterprise. Command centre type products are not new in the market, with products available from vendors such as Philips, Siemens Healthineers and GE HealthCare. However, at this time, there is no enterprise imaging use case – with current products aligned to radiology or enterprise operations as opposed to a broader imaging focus.

What’s Next for Best of Breed Vendors?

As speciality markets converge and the opportunities for IT intertwine, what does this mean for the best of breed (BoB) vendors already occupying the market?

In most instances, larger radiology IT vendors will be seeking a partner, to leverage the BoB brand recognition, specialist tools and overall expertise in the individual market, whether that’s pathology, oncology, or dermatology. Therefore, for BoB vendors, the priority short-term will be finding the right partner(s) to integrate and target larger EI deals. Geographical representation and market share, customer segment, the overall portfolio and ability to integrate, broader strategic alignment on cloud and AI will all be important for BoB vendors to evaluate when assessing partners to ensure the “right fit”. This selection will be important, as this creates an opportunity for BoB vendors mid- to long term.

As enterprise imaging momentum grows outside of the core markets of North America and Western Europe, BoB vendors have an opportunity to leverage a radiology IT vendors market presence to expand into new geographies. However, additional investment will be required, with the BoB assessing regulatory requirements, any implication or challenges on reimbursement, and customer requirements in new markets, whether that’s a priority on AI integration, efficiency-based tools, or public cloud deployments.

Striving the Market Forward: A Vendors Role

Although interest is high across North America and Western Europe around enterprise imaging strategy, converting deals can be a challenge. As noted in the graph above, opportunities over the forecast period are expected to be heavily weighted towards radiology and cardiology. Broader expansion is often set back due to market education; what is the best way to adopt an enterprise imaging strategy? What is the value and use case of having smaller specialities such as point of care ultrasound (POCUS), dermatology, or ophthalmology integrated into an EI strategy? As well as overcoming the inherent departmental and siloed budgets that make a large EI deployment challenging to fund.

The journey to enterprise imaging will be unique to each healthcare provider, based on specific pain points, contract renewals and vendor incumbents for example. However, vendors have an opportunity to drive the market forward. Ongoing industry discussions help, but there remains limited visibility on real-world use cases to allow providers to learn from one another, or a framework on best practice to improve the management and roll-out of an enterprise strategy. This is where technology vendors should focus.

Investing in the Future

Undoubtably, opportunities for enterprise imaging are increasing, with many radiology IT deals evolving to include reference to multiple specialities. Although providers may not be ready for a full enterprise imaging deployment today, providers are seeking a long-term partner that can offer the EI capability when the institution is ready, hence the importance for vendors to invest in platform capability and partnerships now, ready for the future.

However, who will be in the best position to take advantage? The success of an IT vendor will depend on three critical factors: an adaptive sales team, leveraging relationships across the enterprise; class-leading interoperability interfacing across all leading diagnostic verticals; the ability to clearly demonstrate the economic and diagnostic and clinical outcomes and tangible benefits to each care pathway.

Related Research

Market Opportunities for Enterprise Imaging – 2023

A component report from our “Imaging IT Market Intelligence Service”. This topical report assesses the market opportunity for enterprise imaging. Detailed analysis and quantitative summary of EI adoption, evaluating priorities for different ‚Äòologies and timelines for integration, its impact on product development, combined with our strategic assessment on the role EI will play in imaging IT procurement.

Imaging IT Market Intelligence Service – 2023.

The “Imaging IT Market Intelligence Service – 2023” is an annual subscription inclusive of five deliverables. The reports provides full coverage of the global informatics ecosystem and is comprised of detailed global market data and forecasts, alongside qualitative analysis to evaluate key strategic questions.

About Amy Thompson

Amy joined Signify Research in 2020, and is now the Research Manager for Healthcare IT, focusing on imaging and clinical IT, AI in medical imaging and teleradiology. Prior to that, she brings four years’ experience as a Senior Analyst; supporting business strategy and market sizing.

About the Medical Imaging / Imaging IT Team

Signify Research’s imaging IT service provides expert market intelligence and detailed insights across radiology IT, cardiology IT, and advanced visualisation IT, alongside operational workflow & business intelligence tools. Combining primary data collection and in-depth discussions with industry stakeholders, our thorough research approach yields credible quantitative and qualitative analysis, helping our customers make critical business decisions with confidence. Throughout the course of 2023/24, the imaging IT team will be further assessing developments in the market through its’ Imaging IT Market Intelligence Service.

About Signify Research

Signify Research provides healthtech market intelligence powered by data that you can trust. We blend insights collected from in-depth interviews with technology vendors and healthcare professionals with sales data reported to us by leading vendors to provide a complete and balanced view of the market trends. Our coverage areas are Medical Imaging, Clinical Care, Digital Health, Diagnostic and Lifesciences and Healthcare IT.

Clients worldwide rely on direct access to our expert Analysts for their opinions on the latest market trends and developments. Our market analysis reports and subscriptions provide data-driven insights which business leaders use to guide strategic decisions. We also offer custom research services for clients who need information that can’t be obtained from our off-the-shelf research products or who require market intelligence tailored to their specific needs.

More Information

To find out more:

E: enquiries@signifyresearch.net

T: +44 (0) 1234 986111

www.signifyresearch.net