Written by

Share article:

The Global Ambulatory Diagnostic Cardiology Market is evolving at a rapid pace, driven by technological developments, and shifting models of healthcare service delivery and funding. The overall market will grow from $2.5 billion in 2021, to $3.3 billion by 2026, with Long-Term ECG and, to a lesser extent, Mobile Cardiac Telemetry (MCT), being the principal engines of growth. Unsurprisingly, these two markets are garnering serious attention from large incumbent vendors in the more established Implantable Cardiac Monitor (ICM) and traditional diagnostic cardiology markets.

Expanding old horizons through M&A

As health systems around the world seek to relocate more healthcare provision from acute to ambulatory settings, traditional health technology vendors risk being left behind in the old paradigms of care. In response, many have sought to reposition themselves via strategic Mergers & Acquisitions (M&A).

Philips has gone further than most in this regard. Its acquisitions of BioTelemetry and Cardiologs, in 2020 and 2021 respectively, have given it the broadest footprint across the Ambulatory Diagnostic Cardiology landscape, complementing its existing strength in the hospital-oriented Resting and Stress ECG, and ECG management services markets. BioTelemetry also gives Philips exposure to the complementary Remote Patient Monitoring (RPM) market, while Cardiologs AI platform presents an opportunity for future integrations with ICMs (the one market Philips is not in), and the rapidly expanding consumer wearables space.

Other high-profile cases of portfolio expansion via M&A include Boston Scientific’s $925 million acquisition of Long-Term ECG and MCT vendor, Preventive Solutions, and Baxter’s $10.5 billion deal for Hill-rom, both in 2021. The Preventice transaction was part of a rapid ascent for Boston Scientific in the Ambulatory Diagnostic Cardiology market, having quickly grown its share of the ICM market since it received regulatory clearance for its first ICM device in 2020. Baxter also entered new territory in its acquisition of Hill-rom. Previously being a large player in the short-term ECG market, Hill-rom expanded its own solutions portfolio into Long-Term ECG by acquiring BardyDx in early 2021.

Blurring the boundaries – partnerships and emerging technologies in cardiac care

A flurry of recently announced partnerships, some in combination with funding, also hold the potential to dramatically alter Ambulatory Diagnostic Cardiology. Perhaps reflecting an earlier stage of market development, and recent tightening in financial markets, partnerships appear more common than M&A in the emerging fields of hand-held and consumer wearable-based ECG devices.

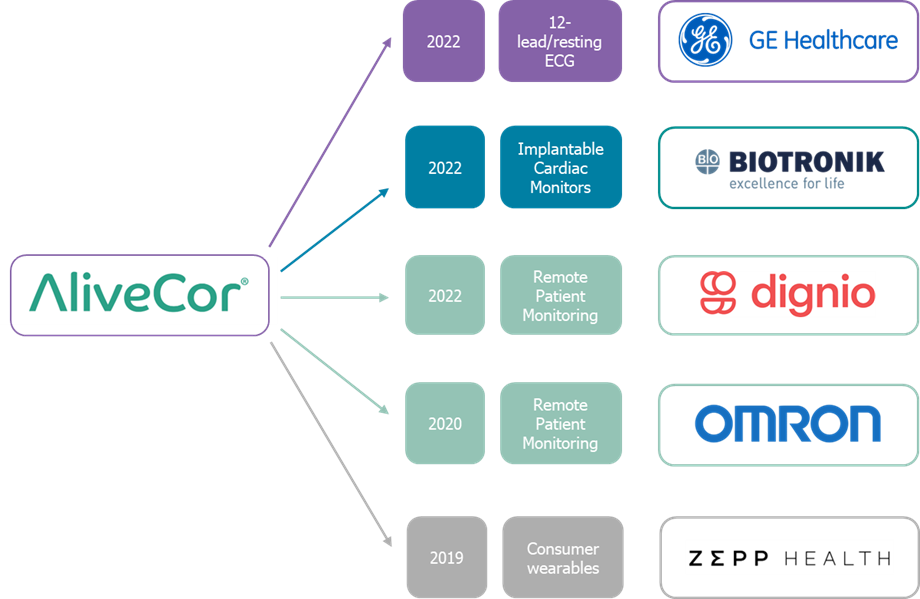

Handheld ECG vendor AliveCor has been particularly active in this regard. Its partnerships with GE Healthcare, the leading player in the traditional diagnostic cardiology markets of Resting and Stress ECG, enables the integration of patient data from AliveCor’s handheld KardiaMobile 6L ECG data directly into GE Healthcare’s MUSE Cardiac Management Systems. In a similar vein, its partnerships with Biotronik facilitates the integration of KardiaMobile and Biotronik’s ICM devices. This could prove to be a canny move for both parties, given that Biotronik currently competes in the oligopolistic ICM market in which its three competitors, Abbott, Boston Scientific, and Medtronic, have a combined market capitalisation of $368 billion.

AliveCor has also established agreements with medical device company (and recent RPM market entrant) Omron, Norwegian RPM vendor Dignio and consumer wearable company Zepp, (though an early integration with the Apple Watch has descended into acrimonious and costly litigation).

Another partnership looking to exploit the potential of ECG sensors in wearable devices is that between iRhythm, the second largest player in the market (when excluding ICM revenues) and Alphabet subsidiary Verily. In July 2022, iRhythm and Verily obtained FDA approval for their jointly developed Zio Watch and Zeus System, for identifying and monitoring Afib, incorporating iRhythm’s continuous PPG, AI-based algorithm. How this partnership will be affected by the recent announcement of layoffs at Verily remains to be seen.

Other companies to enter the fray include multinational tech firms Huawei and Samsung, specialist GPS technology company Garmin, and French connected health company Withings. Interestingly, one of the conditions of Withings’ FDA approval for its ECG-capable ScanWatch stipulated that the ECG feature can only be unlocked by a prescription from a healthcare provider.

Future Outlook

Despite this flurry of activity, the Ambulatory Diagnostic Cardiology market refuses to sit still. Upcoming developments that could disrupt the market over short-to-medium term include a hand-held, 12-lead capability ECG device from Heartbeam, and a multi-modality cardiac monitor (Holter(short-term and Long-term ECG), Event and MCT) with built-in 4G connectivity from Rhythmedix, both US-based vendors. A domestic vendor in India, Dozee, recently released an ECG patch, while South Korea is also host to a number of Long-term ECG patch vendors in the process of international expansion. A new cohort of vendors in Europe and the US are also looking to exploit the potential of AI for quicker and more accurate diagnosis.

Ongoing advances in adjacent technologies and markets, such as Remote Patient Monitoring (RPM), and consumer devices, will also continue to influence the Ambulatory Diagnostic Cardiology market. The Long-Term ECG market in particular, where technological advances have lowered barriers to entry, will likely see a proliferation in vendors over the short-to-medium-term. However, as is the case in all healthcare technology and software markets, providers continue to favour dealing with a small number of large vendors who can offer enterprise-level solutions (including ongoing technical and administrative support). Without this protective umbrella, vendors supplying specialist, single-point solutions may struggle to achieve critical mass. This suggests yet more M&A and partnerships involving the large traditional vendors are to come.

Of the current crop, Philips, despite recent travails in its wider business, has the most comprehensive ambulatory diagnostic cardiology solutions offering, though newly independent GE Healthcare has already signalled its intentions to expand into ambulatory and remote care. Baxter, post its Hill-rom acquisition, has also established a presence, though it is yet to achieve substantial market share.

Of the major ICM vendors, only Boston Scientific and Biotronik have made significant recent moves, while the contribution of Abbott’s ICM business to overall revenue is minimal. Medtronic, the proverbial 800-pound gorilla in the ICM room, is in the midst of a major restructuring, including the spin-off of its patient monitoring and respiratory interventions businesses, but has surely been watching recent developments with more than a passing interest.

All of the this points to more partnerships, more M&A and more disruption to come, meaning the Ambulatory Diagnostic Cardiology market will remain one to watch in 2023 and beyond.

About the Report

“Ambulatory Diagnostic Cardiology – World – 2022” provides a data-centric and global outlook of the Ambulatory Diagnostic Cardiology Device and Service (ex. ICMs) market. The report blends primary data collected from in-depth interviews with healthcare professionals and technology vendors, to provide a balanced and objective view of the market.

About Signify Research

Signify Research is an independent supplier of market intelligence and consultancy to the global healthcare technology industry. Our major coverage areas are Healthcare IT, Medical Imaging and Digital Health. Our clients include technology vendors, healthcare providers and payers, management consultants and investors. Signify Research is headquartered in Cranfield, UK. To find out more: enquiries@signifyresearch.net, T: +44 (0) 1234 436 150, www.signifyresearch.net

More Information

T: +44 (0) 1234 986111

www.signifyresearch.net